Ongoing threats to vessels transiting in the Suez Canal and the severe drought conditions in the Panama Canal, continue to significantly impact global ocean freight transit times and costs. While more capacity has been released, current volumes cannot meet the current demand pre-Lunar New Year.

RED SEA - STATUS UPDATE

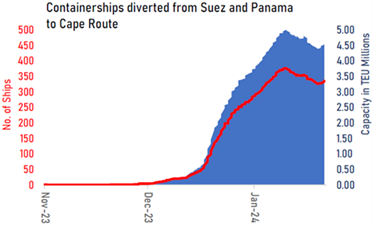

As of February 1, 80% of all containerships (or 300+ vessels) on the Suez route have diverted to the Cape of Good Hope. This number is expected to increase as more vessels continue to reroute.

- This rerouting has caused 7-14 days additional transit time and 15-20% higher cost on surcharges.

- While a majority of the impact is being felt on Asia-to-Europe Trade, there is a knock-on impact for Transpacific Routes. Panama Canal restrictions had caused earlier diversions to Suez which have now gone around Cape of Good Hope.

RATES & CAPACITY

- SCFI rates made its 8th consecutive weekly gain with spot rates rising by over 340% since November on the back of the Red Sea crisis.

- Spot rates to both the West Coast and East Coast rose by over 40% last week.

- The rate gains far outweigh the incremental costs from the Cape diversion, with estimates ranging from just $100 to $150 per teu, coming mainly from higher fuel expenses together with increased vessel and equipment costs which are partially offset by savings from Suez Canal fees.

- By trade lane

- S. West Coast lanes – Carriers are switching ships away from the US West Coast to Europe where the vessel shortage will become more acute and thus USWC rates are increasing

- S. East Coast Lanes, All cross Suez services will incur additional transits approximately 7-8 days. While Panama canal transits remain restricted through Jan to only 24 vessels / day.

- European Union lanes, capacity utilization dropped slightly due to a higher-than-normal week 1 capacity available, but this will reverse in the next few weeks with the capacity shortfall expected to peak in weeks 5 and 6.

ONE MORE INSIGHT - CONTAINER EQUIPMENT AVAILABILITY

This will mean increased transit times and rate volatility for shipments moving from Asia to Europe, and Asia to the US East Coast.

- Container equipment availability is expected to be short by March 2024 –

- As of Jan. 1, 2024 the cellular container fleet comprised 5,977 ships for a total capacity of 28.13 Mteu. This represents a year-on-year net increase of 271 ships and 2.14 Mteu - or 8.2%.

- Inactive containership capacity has also fallen sharply in the last 2 months, with idle capacity at just 82 ships for 138,000 teu currently.

- With additional demand stemming from Lunar New Year, we could be facing a shortage of availability.

THE BOTTOM LINE - EXPECT DISRUPTIONS TO PERSIST

The situation in the Red Sea remains precarious, and the effects of global warming on the lowering of water levels in the Panama Canal will be long-lasting. Carriers will continue to reassess the situation regularly before reinstating their services. Until then, the industry will continue to have to contend with higher costs, longer transit times, and environmental concerns.

WHAT's next?

We are continuing to monitor the situation closely and provide timely updates to those impacted. At this time, your SEKO team advises that you and your team:

- Plan for long-term contracts carefully: In light of fluctuating freight rates and uncertain transit times, approach long-term shipping contracts with caution.

- Build out buffers again: We are planning for potential delays and disruptions, and you should, too. Manage your customers’ expectations to help maintain proper inventory levels during challenging times.

- Collaborate with logistics partners: Maintain close communication with your logistics providers. Their expertise and resources can be invaluable in navigating these challenges and finding the most efficient shipping solutions.

- Explore multimodal transportation options: Consider combining different modes of transportation (sea-air, expedited ocean, Mini Land Bridge) to optimize your shipping routes. This approach can offer more flexibility and potentially reduce transit times.

- Send your forecasts often: Send accurate forecasts (including container type and counts) to plan for February and March capacity as soon as possible.

We are your logistics partner, ready and able to pivot quickly in the face of logistics challenges, whether climatic (as we’re seeing in the Panama Canal) or man-made (as we’re seeing now in the Red Sea). Should diversions persist or expand, our team is prepared to help find alternative routes, where necessary and create a solution that works for your business and your customers.

Reach out to your SEKO BANSARD representative or email us at sales@bansard.com